Which payments bank should you choose and why? Here’s a comparison of the features offered by three payments bank in India.

Paytm Payments Bank officially started operations earlier this month, becoming the third player in India. Although the Reserve Bank of India gave in-principle nod to 11 entities, many have dropped out or delayed their launch.

According to Satish Meena, senior forecast analyst at Forrester Research, the reasons why other entities have dropped out while Paytm has launched its Payments Bank is that it has a platform to offer multiple layers of financial services.

Role of a Payments Bank

A payments bank can accept deposits of up to Rs. 1 lakh per customer in a savings account current account, offer debit card and online banking. However, it cannot advance loans or sell credit cards.

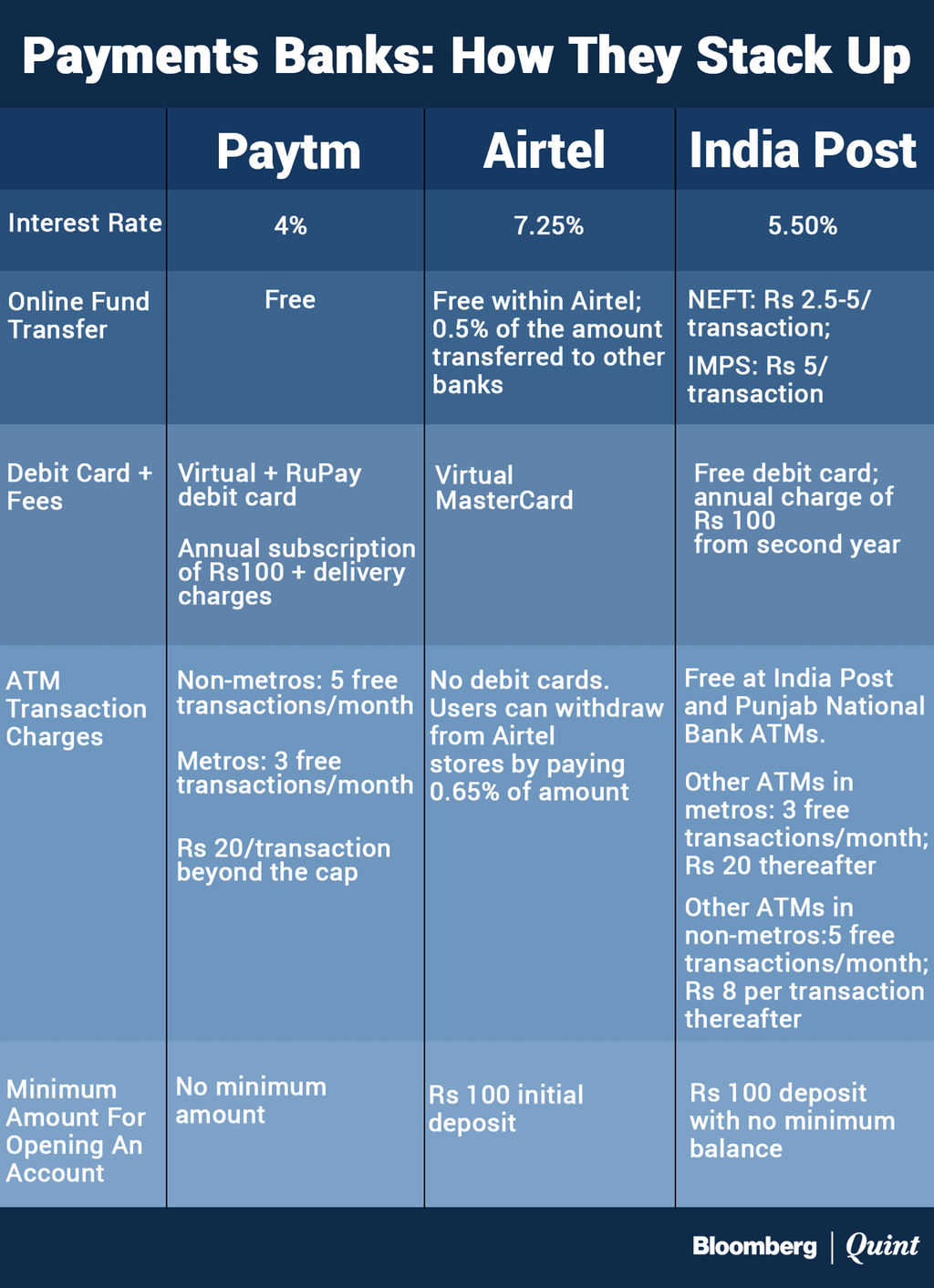

Let’s take a look at the various features offered by the three Payments Banks in India: Paytm vs Airtel vs India Post.

Interest Rate

Airtel Payments Bank offers 7.2 percent, the highest interest rate on deposits, followed by India Post which offers up to 5.5 percent. Paytm offers the lowest rate, 4 percent, in line with large commercial banks like HDFC Bank Ltd., ICICI Bank Ltd. and Axis Bank Ltd.

Debit Cards

Airtel’s payments bank does not offer a physical debit card, while Paytm will provide RuPay debit cards at an annual subscription cost of Rs 100 in addition to delivery charges. India Post is offering free debit cards, but charges Rs 100 for an add-on card.

In case of loss of card, Paytm will charge Rs 100 plus delivery charges. The bank is also providing a cheque book at Rs 100, plus delivery charges, for 10 cheque leaves.

India Post charges an annual maintenance fee of Rs 100, which is applicable from the second year onwards. In case the ATM kit or ATM card is returned due to a wrong address, the customer will have to pay Rs 100 as replacement charges.

Online Banking

Paytm’s payments bank will provide free online fund transfer services such as Immediate Payment Service (IMPS), Unified Payment Interface (UPI) and National Electronic Fund Transfer (NEFT).

India Post will charge a fee if the transaction happens at the branch. NEFT will cost Rs 2.5-5 per transaction, while an IMPS transaction will cost Rs 5. For mobile banking, NEFT is free but IMPS is charged at Rs 4 per transaction.

Airtel charges 0.5 percent of the amount if funds are transferred to another bank account through internet banking, mobile app or Unstructured Supplementary Service Data (USSD). Within the bank, fund transfers are free.

Cash Withdrawal Charges

Paytm’s payments bank users will get five free transactions in non-metro cities and three in a metro, after which they will be charged Rs 20 for each cash withdrawal and Rs 5 for non-financial transactions like taking out a mini-statement. For a physical statement, customers will have to pay Rs 50 plus delivery charges and service tax.

Airtel will levy 0.65 percent of the amount for a withdrawal from a banking point.

India Post will not charge any fee for withdrawals at its own or Punjab National Bank ATMs. However, for withdrawals from other banks’ ATMs, users will get five free transactions per month in non-metros and three in metros. Beyond that, it will charge Rs 8 and Rs 20 per transaction, respectively.

Sponsored Services: Zintego remittance receipt sample

Leave a Reply