This article discusses the locker facilities provided by banks in India and their features. Here you will also get to know how banks have been unfair on certain practices with regards to the locker allotments and what RBI has to say on this.

Bank Lockers in India: Significant Features

Just like we trust a bank with our money in savings account or fixed deposits, we have bank lockers to safeguard our valuables such as jewelry, important documents, property will etc.

Bank lockers are a safe and secure option to store important items which are quite unsafe at home. Besides, they offer long-term protection.

These are industrial strength storage compartments which ensure maximum safety of your important belongings. And these are mostly manufactured and supplied by Godrej.

Each locker has two keys; one remains with the customer and the other with the bank. The locker opens when both the keys are used. The bank officer applies the key first and leaves the locker room. Now it’s your turn. You can use your key and operate your locker.

Who Can Avail Locker Facility in Banks?

Usually, the locker facility is made available for the existing customers.

Although banks cannot deny the non existing customers, having a bank account is often like a pre-requisite in the pretext of getting the KYC done.

Individuals, limited companies, associations, trusts etc. can avail bank lockers, where as minors are not eligible for this.

Availability of Locker

For many banks, the locker facility is provided at select branches. And the allotment of locker is made on “first come first serve” basis.

If none is available, banks should maintain a wait list for the purpose of locker allotment. All customers, who are looking for locker, must be acknowledged and given a wait list number. Besides, the bank must inform them when the locker is available. Overall, banks are supposed to maintain transparency in this regard.

Locker Rent

The locker rent per annum depends on three things,

- Size of the locker(dimesion)

- Location of the branch(Urban, Semi urban, rural)

- Type of bank (public or private banks)

Lockers come in different dimensions. Customers can choose what fits their requirements and the rent varies accordingly.

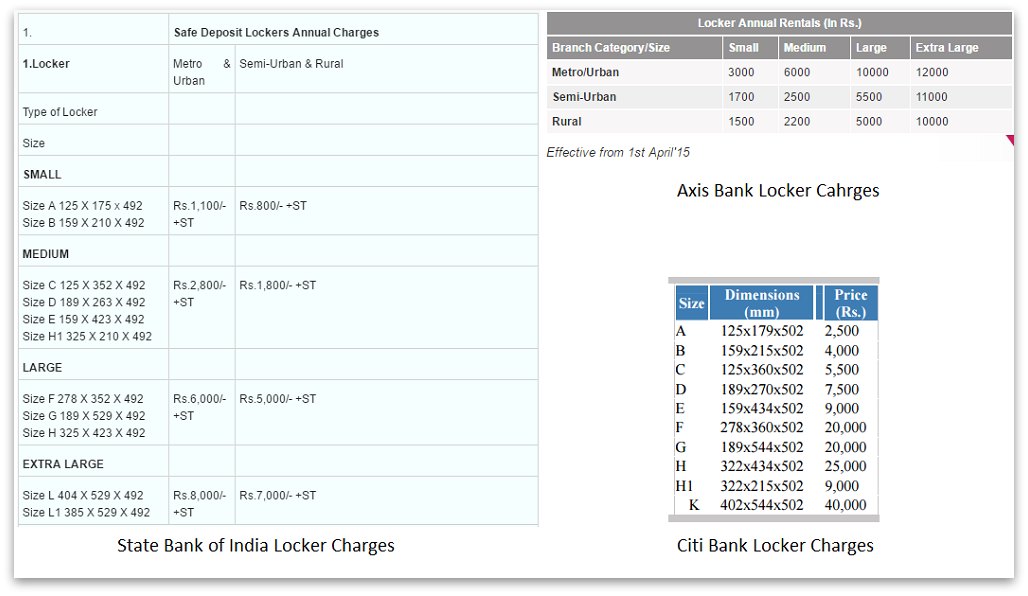

The locker rent in private banks is usually steeper than in public sector banks. For example, Citi bank charges around Rs.2500 for the smallest locker and Rs.40000 for the largest ones. Where as in State Bank, the locker charges begins from Rs.800 in semi urban and rural branches and Rs.1100 in metro and urban excluding the service tax.

(The snapshots of webpages are taken on 17th May 2016)

Banks take a one-time registration fee. Besides, they can charge you on visits beyond the free ones. The number of free visits a year is usually fixed and limited. For example in Bank of Baroda, you can operate a locker 12 times in year for free. Visits beyond that will cost Rs.100 per occasion.

Fixed Deposit as Security for Locker

When a customer approaches a bank for locker facility, banks ask them to create a fixed deposit as a security for locker.

Although this is to compensate the locker costs, in case the customer doesn’t pay off the locker rents for long, customers are likely complain when the amount of fixed deposit is too much.

There have been several instances when banks demand a hefty amount of FD for this purpose. Certain banks force customers to buy ULIPs or other investment products calling it a part of the locker allotment policy. Truth to be told, this is a violation of RBI rules.

So what do you think is right? Is it really necessary to have a fixed deposit in order to get a locker?

RBI answers it this way,

“1.2 Fixed Deposit as Security for Lockers

Banks may face situations where the locker-hirer neither operates the locker nor pays rent. To ensure prompt payment of locker rent, banks may at the time of allotment, obtain a Fixed Deposit which would cover 3 years rent and the charges for breaking open the locker in case of an eventuality. However, banks should not insist on such Fixed Deposit from the existing locker-hirers.”

Hence, the correct amount of fixed deposit for locker security in a specific bank= Locker rent (incl. service tax) for 3 years + break-open charges of the locker

For example, if the locker rent per annum is Rs. 1500 including service tax and the breaking charge is Rs. 500, the bank shoud ask you to open an FD of Rs.5000 (1500×3+500). Not more than that. Asking for high amount FD is an unfair practice and it should be stopped immediately.

Certain public sector banks like Bank of Baroda clearly mentions the rules on the websites,

“At the time of hiring the locker, bank will obtain a minimum-security deposit in the form of FDR from the lessee for the amount which would cover 3 years rent and the charges for breaking open the locker in case of such eventualities.”

So the next time you visit a bank and face the situation, you can remind the bank of the guidelines laid down by RBI.

Nomination and Joint Account Locker Facility

Both ‘nomination’ and ‘joint account’ facilities are available for bank lockers.

In fact, if you’re availing a bank locker it’s always advisable to have it in joint holders’ names or assign a nominee. So that when one person is unavailable other person can operate the locker.

In case the primary account holder dies, the nominee can access the locker after providing necessary documents.

Breaking Open of Lockers

Banks can break open the lockers depending on several situations. If you are not paying off the locker rents despite multiple notices from the bank, they can break open the locker as per the bank’s norms.

Further, depending on the risk factor you are assigned with, you have to operate the locker from time to time. If it has been really long since your last locker visit, banks may take necessary actions in this regard.

Therefore, if you have genuine reasons that you can’t operate the locker for quite a long time, you should inform the bank and cite the reasons.

How Safe are Locker? What happens when something goes wrong?

Bank lockers are just professional arrangements to provide the best possible security to your valuables. Whereas banks are in no way responsible if something happens to the content of your locker, not even in the event of robbery or natural calamity.

Also, there have been few instances of termite attacks despite the high quality safe which often goes through rigorous safety test.

As far as the compensation goes, bank is not liable to any.

However, if the banks are found irresponsible and not providing adequate security or the basic maintenance, then you could definitely get some compensation by moving to the court.

Considering this, we can never say bank lockers are 100% risk free, especially when bank doesn’t compensate for the loss. But keeping valuable items at home is not safe either.

Risk will always be there. How you handle it, makes the difference. At the ending note, here are some simple, useful tips your disposal.

- Wait till the bank officer with the second key leaves the locker room. When you open the locker, make sure there’s no one around. When you are done, locked the safe properly before leaving.

- Make sure your bank has installed all the necessary security measures, such as CCTV, alarm system etc.

- Visit the locker from time to time and check your valuables.

- Choose a bank on the basis of its proximity. So you can visit the locker more conveniently.

- If you are keeping papers or documents, better have them laminated before putting in there.

- Make a note of what you have stored in the lock. Also write down your visiting dates.

- Go through the bank’s guidelines on locker.

These are some best practices you should follow while availing/operating a locker. Remember, banking ombudsmen and RTI are always there to protect your rights. You should never let anyone exploit you.

Recommended Readings:

Are Bank Lockers totally Safe & is Fixed Deposit really required to get one?

5 things to keep in mind while renting a locker

Leave a Reply